I was moved to tears when I first stumbled upon this video. As a child I grew up in a verbally abuse household and despite my wanting to be a less angry person, I have unfortunately been shaped by negative experiences both inside and outside of home. Stress has led me to eating more and more to deal with it. I sometimes forget to think and swear angrily which has obviously led to more family escalations. I try to retreat away and punch the wall or hit myself to calm myself down. I now have high blood pressure as well.

I have always wanted to avoid having children because I fear that my violent conditioning may show up again as a parent. I also avoided relationships because I don't want the person I love to see me when I'm in a terrible state. I never knew how to focus my frustrations and anger as a child. Its taken many years, with the help of music and the internet to help me understand mental health and anger as a topic more closely.

When I watched this video I felt hopefully that there is hope for children out there and even myself. As an adult I should try my best to teach this to children when I see an opportunity. Its fascinating to think that children so young can have a grasp on mental health issues such as these. Then again they are slowly learning about the world and themselves. They come up with very colourful metaphors and solutions. I especially liked the idea of the mind as a jar of glitter that gets shaken up. I was also pleasantly surprised by the child who knew how anger is processed through the pre fontal cortex.

Dear reader, please take a few minutes to watch this very touching and informative video.

The government will impose GST on "intangible" products such as downloads and online streaming as well as extending it to imported parcels worth less than the current minimum of $1000.

Bank deposits tax

Tax on bank deposits that will raise about $500 million for a fund to be used in the event of a bank collapse. The fund will also be factored into the budget balance sheet.

Not-for-profits to lose perks

Workers in the not-for profit sector will have their fringe benefits tax exemptions tightened. The move - capping the amount they can claim on meals, holidays and other expenses - aims to save the government $300 million over four years.

ABS boost

The Australian Bureau of Statistics will receive a funding boost of $250 million for a massive technology upgrade. The census will also be saved from the chopping block.

Mental health funding

$300 million in funding to mental health groups has been granted a last-minute extension of one year. The funding, directed to organisations like Lifeline and ReachOut, was due to expire at the end of this financial year.

Pensions assets test

Many wealthier retirees will have their part-pensions reduced or become ineligible altogether. The less wealthy will see either no change or receive a small boost to their pension payments. These measures are expected to save $2.4 billion over the next four years.

Photo: Louie Douvis

PBS savings

$3 billion in net savings will be sought from the Pharmaceutical Benefits Scheme. $5 billion is set to be saved by measures including price reductions on medicines removing over-the-counter products and a stricter safety net, with $2 billion to be reinvested in other drugs.

Vaccination boost

$26 million will be spent on incentive payments for doctors who vaccinate overdue children. This and denying welfare payments and rebates to parents who don't vaccinate their children aim to boost vaccination rates.

Photo: Sean Gallup

Big cash to WA

Western Australia will receive a one-off payment of $499 million to make up for its GST shortfall. The money will be used for nine infrastructure projects.

Car industry assistance

Up to $500 million in car industry assistance over the next four years was restored after the government originally announced it was to be removed completely. They expect to spend only $100 million of it.

Photo: Jessica Shapiro

Small business tax breaks

Small businesses and sole traders will receive a 1.5 per cent tax cut, bringing the amount of company tax they pay down to 28.5 per cent. A new accelerated depreciation policy will also allow them to write off up to $10,000 a year.

Start-up incentives

The cost of setting up a business will be reduced. Under the proposal, legal and accounting advice can be immediately written off and the process to register the business will be simplified.

Defence pay

The government, succumbing to political pressure, lifted the increase in defence workers' pay from 1.5 per cent to 2 per cent. This will amount to a $217 million hit to the budget over four years.

Reef protection

An extra $100 million to fund long-term initiatives aimed at protecting the Great Barrier Reef. The plans focus on water quality, coastal development and fishing activities as the biggest threats.

Legal aid funding

The government reversed cuts from last year's budget, reinstating $25 million over two years for community and indigenous legal aid services.

Childcare reform package

Multiple childcare payments will be rolled into one and there will be tougher work requirements for parents wanting to qualify for childcare support. $327 million in new funding will be directed to fund childcare for families in remote areas and those at risk. $246 million in funding will be provided for about 4000 nannies in a year-long trial.

HECS repayments

The government will pursue university debt repayments from graduates living overseas, expected to recoup $14 million a year.

Photo: Andrew Quilty

Fight against Islamic State

Australia's military presence in Iraq is set to cost more than $400 million per year.

Foreign aid

Australia's foreign aid contribution is to be slashed by $1 billion, scheduled as part of last year's budget.

What's been ruled out and abandoned

"Google tax"

Not to be confused with the "Netflix tax", the proposed Google tax would have imposed a 30 per cent tax on profits earned in Australia by multinational corporations.

Superannuation tax hikes

The government has ruled out major changes to superannuation tax breaks that mainly benefit wealthier people. Independent analysis estimated that this will cost the budget $6 billion a year.

Medicare co-payment

The $7 fee on visits to the GP originally proposed in last year's budget has been officially scrapped after facing stringent opposition, even after various concessions.

Extending budget repair levy

The temporary two per cent levy on incomes over $180,000 will not be extended past the promised the three years, despite collapsing government revenues.

Curbing negative gearing

The government will not attempt to wind back negative gearing on investment properties, although it was briefly discussed.

Pension indexation

Originally proposed in last year's budget, the government will no longer attempt to lower the indexation rate for pensions.

Hangovers from the 2014 budget

Cuts to the dole

Tough measures, including the six-month wait for the dole, were meant to cut $3.9 billion from welfare spending. Despite stiff opposition, the savings are being included in the upcoming budget.

Tightening of disability pension

People under 35 were expected to face tougher criteria to remain on the pension, with the focus on those who can work and be integrated back into the workforce

Uni fees deregulation

It was expected that university fees would be uncapped, increasing the debt burden for many students. Originally intended to save $3.6 billion, this was reduced to $930 million after various concessions.

Family Tax Benefit crackdown

Billions in cuts to to family tax benefits are still being factored into this year's budget, despite facing rejection in the Senate.

[YEAH SORRY THIS IS MOSTLY INFORMATION FOR MYSELF BUT HEY IF YOU'RE IN AUSTRALIA AND WANT A HOUSE THEN TAKE A LOOK AT THIS YO]

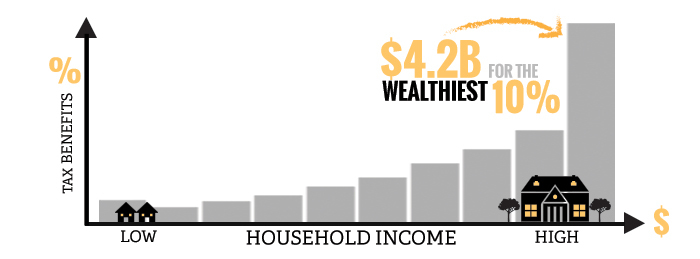

It's time to tighten up negative gearing

Negative Gearing costs the government billions ever year; it reduces homeownership; and it increases inequality. In fact, The Australia Institute's report – fully funded by GetUp members – shows that $4.2B in negative gearing tax breaks go to the top 10% of income earners.

There's growing consensus that it's time to reform negative gearing – from the Chief Economist at Bank of America Merrill Lynch to the Australian Council of Social Services. And it's not hard to see why: in one fell swoop we could have a fairer budget that saves the bottom line billions and makes housing more affordable.

We need a Brighter Budget that gets rid of unnecessary, wasteful handouts for the wealthy. Will you sign on to join the Brighter Budget campaign and help champion smart, fair solutions for this year's Budget – such as negative gearing reform?

Negative gearing operates as a tax break for investors. For property investors, this means using their rental property costs to reduce their taxable income. (E.g. If the costs-associated with your property are higher than the earnings from your poperty (rent), you can use that loss to pay less income tax.)

It may seem complicated, but it's very simple when it comes to who wins and who loses.

The winners are the wealthiest 10 per cent of income earners who receive the vast majority of the tax break.

The losers are the low income earners, who are shut out of an already hot housing market, with negative gearing fanning the flames.

But in the end, all Australians lose. With negative gearing, the government is wasting potential revenue on wasteful tax breaks for the wealthy. This money could instead be spent on services we all need, like better schools and hospitals.

It's also important to remember that Australia is one of the few countries to allow negative gearing losses to directly offset your taxable income. It is far more restricted in Britian, and even the United States.

One possible solution is to reform negative gearing so that it applies to new construction only – this is the crux of the Australia Institute's report. Doing so would create more of an incentive to invest in new housing, therefore increasing supply and driving down prices and rent.

The Government and the Labor opposition are looking for ways to save money in the Budget — so GetUp members are getting on the front foot to ensure these savings are fair and sustainable over the long-term. Instead of the austerity cuts that attack everyday Australians, we're campaigning for a Brighter Budget this time around.

Here are the policies we're launching as part of our Brighter Budget campaign:

Reform negative gearing. Restrict tax concessions for negative gearing so they only apply to new housing stock. Australia is one of the few countries to allow negative-gearing losses to be offset against income – and no wonder given that fifty percent of this tax break goes to the top two percent of income earners. Reforming negative gearing will encourage investment in new housing stock, put downward pressure on rent and make housing more affordable.

Reform superannuation tax concessions. Instead of giving all the tax breaks to those at the top, give the bigger concessions to those who need them most, and in the process ensure everyone can save for their retirement. Click here to sign the petition.

Introduce the 'Buffett Rule'. Thanks to tax loopholes and high priced accountants, Kerry Packer famously reduced his effective tax rate so he paid less tax than his gardener. 'The Buffett Rule' would put a cap on loopholes for the top 1% of income-earners to ensure they pay at least the same tax rate as middle-income Australians. Click here to sign the petition.

Scrap the capital gains tax discount. Concessions on capital gains tax predominantly benefit the wealthy, who have a larger proportion of their income from investments. Getting rid of the discount could save about $4 billion.

Cut fossil fuel subsidies. Right now, the government hands over $11.5 billion a year in industry subsidies that incentivise pollution. We need to cut industry subsidies that aren't actually helping to create jobs and are just giving a hand out to multi-million dollar companies whose profits go overseas.

Impose a super profits tax on banks. The big banks make inflated profits thanks to a lack of competition. A tax on those super profits would help compensate Australians for higher fees and charges.

Introduce a 'Tobin Tax' on high frequency financial transactions. Big investment banks use powerful computers to trade in the financial market at huge volumes. This high frequency trading pushes up share prices for normal mum and dad investors. A tax of less than half a percent on these big investment banks' transactions would improve market stability and raise over $1 billion a year.

Place a duty on wealthy estates. Place an inheritance tax on large estates.

I find it very hard to learn something unless I'm truly interested in it and i want to learn.

Learning about things like tax, housing, economics these things are absolutely essentially but because I'm a lazy bastard i tend to ignore it

But as a social worker I should engage more with how social and economic structures affect people. That is after all going to be my job. Therefore i DO have an interest in learning about these things. After all I'm going to be affected as well

I've heard a lot about a term called 'negative gearing' recently so i decided to look around.

What i found was shocking but not unexpected considering how much the government doesn't care about transparency and prefers to torment those at the bottom of society, welfare recipients, single parents etc.

I'm leaving this here for myself and anyone else who lives in Australia and wants to know about what negative gearing is, how its messed up and raised the housing prices in Australia, making it unaffordable unless you're filthy rich

You know? i might just make a series out of this "Woes of learning about the system"

How tax breaks for investment properties have created a housing affordability crisis while lining the pockets of those least in need.

David is just the sort of motivated, self-reliant bloke that our political leaders like to laud.

He had his own business for 30 years as a freelance graphic designer in Melbourne. He’d never been on welfare. He was a lifter not a leaner, to borrow the tendentious slogan of the Abbott government.

Then his marriage broke up. He left for country Victoria, bought some land, planned to build a new house and a new life. He remarried and had a new family.

But things went bad. The land flooded, the work dried up. Now, at age 53, he has been on unemployment benefits for a couple of years.

He says he is “desperate” to find work, but David (not his real name) is stuck. There might be work back in Melbourne, but how would he afford the rent? Even the dilapidated old farmhouse in the country where he now lives eats up well over half of his meagre welfare payments.

“Like most people,” he writes, “we aspire to home ownership and to leave some kind of inheritance for our children, but I have come to see that in the current climate this aspiration is a mere dream for many people.”

He continues: “It’s not just a young person’s or a first-home buyer’s problem, it affects people of all ages – including older people like myself who have previously owned a share of real estate, but who have fewer working years remaining to better their situation.”

David is no fool. He has studied the analyses by welfare agencies and economists, the statistics from the tax office, and he knows exactly why housing is increasingly unaffordable, not just for welfare recipients and renters like himself but for millions of working Australians.

He understands that it’s caused by loopholes in the tax system that encourage, in his words, “greedy investors [who] compete with the poor and first-home buyers and create artificial demand, which in turn flows right through the whole housing sector”.

Treasurer Joe Hockey should know how the system works, both in his role as treasurer and through personal circumstance, given that his family owns several investment properties. Yet he continues to argue tax breaks given to property investors make housing more affordable, all evidence to the contrary.

Referring to negative gearing, through which property investors can claim as losses the financing and other costs of their rental properties against their other income, here is Hockey on Adelaide radio on Tuesday: “If you were to remove negative gearing you would see an increase in rents, and I think that hurts lower-income Australians who may be renting those homes.”

Hockey went on to voice another contentious proposition.

“In fact,” he said, “most people who access negative gearing are middle-income Australians.”

The overwhelming majority of independent analysts argue both those claims are untrue. Saul Eslake, chief economist for Bank of America Merrill Lynch, goes so far as to call the latter assertion a “lie”.

Housing stress

Back to David. He agreed to be a case study for the social welfare and charity organisation Anglicare’s 2015 rental affordability snapshot, released on Thursday.

“Snapshot” is really too small a term. It is actually a big, depressing panorama of unaffordability.

The survey covered 65,614 properties right across Australia. It used the commonly accepted benchmark of affordability, which is that when housing costs are greater than 30 per cent of the disposable income of a household in the bottom 40 per cent of income distribution, the household is deemed to be in “housing stress”.

Its findings are sobering. For a single person on the age pension, there were fewer than 600 properties in Australia that met the affordability criteria to rent. That’s 0.9 per cent of the total rental stock. For an age pensioner couple, 3.4 per cent of properties were found suitable.

For those on other kinds of welfare it was even worse. For someone on youth allowance, the Anglicare survey found eight properties. For a single person on Newstart allowance, there were 10. These are not percentages; they are numbers. Eight and 10 respectively of 65,000 rental properties in the entire nation were affordable.

Things were but slightly better for the working poor. Only about 2.3 per cent of all rental properties in Australia were affordable for a single person on the minimum wage of a little over $33,000 a year.

For a single parent with two young children, and therefore receiving family payments, the figure was 3.3 per cent. Even for a family with two young children, in which both parents worked for minimum wages, only about 24 per cent of properties were suitable.

The stress of paying high rents, says Anglicare’s executive director Kasy Chambers, means “people are going without things you and I would think non-discretionary, like car insurance, medication, a haircut for a job interview, maintaining the internet for their kids’ study”.

One of those items people went without was food, she said. “You can skip eating for a day, but if you don’t pay your rent you get thrown out. So food becomes a discretionary item. Over 65,000 Australians are living in food insecurity.”

Perhaps you can ignore the plight of the welfare dependent or minimum wage battlers trying to make the rent. Then think about yourself or your children. As David correctly notes, the affordability crisis affects a wide range of people, many of them much further up the income scale.

“There has been a big slide in home ownership for all households under the age of 55 over the past few decades,” says John Daley, chief executive of the Grattan Institute.

“Among those aged 25 to 34 it has fallen from 62 to 48 per cent over the past 30 years. For those 35 to 44 it has gone from 75 to 65 per cent.

“Households on the lowest incomes have done particularly badly. But now even among more middle-income households, those in the second, third, fourth quintiles [i.e., those between 20 and 80 per cent of the way up the income scale], we’ve seen falls of five or 10 points in rates of home ownership among the 25- to 34-year-olds and the 35- to 44-year-olds.”

There are a number of reasons for this. The increasing disparity in wages, for one. More relevantly, rapid population growth through immigration, planning and zoning restrictions and growing numbers of foreign buyers have combined to increase demand and limit supply.

But the big driver of inflated prices, the evidence shows, is speculative investment in rental properties, which has inflated prices.

Even for those of us who manage to buy into the market, this is a problem.

Just this week the credit ratings agency Moody’s released a new study of housing affordability in Australia, showing mortgage costs running at 27 per cent of income, nationally. In Sydney, the figure was above 35 per cent.

Affordability was the lowest it has been since 2008. In reality it’s actually much worse now, for in 2008 the official interest rate went to 7.25 per cent. Now it is a fraction of that: 2.25 per cent.

As interest rates have declined, buyers have simply loaded themselves with more debt. And if rates rise to any significant extent, many will have big problems meeting the cost. A 1 per cent increase in interest rates, Moody’s said, would see Sydney’s affordability decline “by 3.5 percentage points, which is the same as the impact of increasing house prices by 10 per cent”.

Applying the same affordability measure nationally it would increase by 2.7 percentage points.

Yet the property bubble inflates, driven substantially by mad speculation of investors. Increasingly people are taking out interest-only loans to buy real estate. The most recent data from the Australian Prudential Regulation Authority shows that 40,000 such loans were written in the December quarter of last year alone.

Clearly most of these people are not buying properties to live in; 35,000 loans were for investment properties.

Rule changes

Negative gearing has long been a feature of the Australian tax system. But it was only in the late 1970s that investors started using it in a significant way to minimise their taxes by writing rental losses off against their wage and salary income.

In 1985 treasurer Paul Keating changed the rules to stop this, but the policy was reversed just two years later in the face of fierce opposition from the property sector, which ran the line that the law change was pushing rents up.

The argument was entirely specious, as has been demonstrated many times over many years by many economists.

The data shows that nationally rents actually rose much faster both before and after the Keating experiment in quarantining rental losses. But they did rise sharply with the policy in place – entirely coincidentally – in the Sydney market. Labor was desperate to win the 1988 New South Wales election, so it junked the change. It lost the election anyway.

The legacy of that capitulation has been to entrench the argument of the property industry that negative gearing helps keeps rents down, the argument that Hockey continues to trot out with monotonous regularity now as pressure builds to do something about the real estate bubble.

At face value, the claim appears to have some logic – that because they get a tax break, property investors do not have to charge tenants as much.

But John Daley says that is not true. Actually, it simply pushes up prices.

“Negative gearing in effect increases the return on a given dollar of rental income, which means people are prepared to pay a higher price for the asset,” he says.

But negative gearing is only half of the picture.

“The real problem,” says Australia Institute senior economist Matt Grudnoff, “came in 1999 when [treasurer Peter] Costello introduced the discount on capital gains tax. Before 1999, on average, rental properties made a profit.”

But the Costello cut in the capital gains tax suddenly made it vastly more attractive for investors to speculate on real estate, knowing that they could both claim their costs and losses as a tax deduction through negative gearing while they owned the property and reap a much bigger profit when they ultimately sold.

“The net loss from negative gearing just exploded after that,” says Grudnoff. “The net rental loss in Australia is close to $8 billion a year now, and growing fast.”

About a million Australians now own negatively geared properties, but the great majority of them are not, as Hockey claims, the mums and dads of middle Australia.

Analysis this week from The Australia Institute showed that:

• 55 per cent of the benefit of capital gains discount and negative gearing goes to the top 10 per cent of income earners;

• households in the lower half of the income range reap only about 20 per cent of the benefits of negative gearing and slightly more than 7 per cent of the capital gains benefits.

Not only do the benefits flow overwhelmingly to the wealthy and cost the taxpayer – about $7.7 billion last year – they do little to increase the supply of rental accommodation. Some 93 per cent of investment goes into established properties.

Grudnoff would solve the problem by simply doing away with the tax breaks on negative gearing and capital gains tax.

Daley reckons the capital gains tax is the bigger problem: “The first best policy response would be to get rid of the capital gains tax discount.”

If that were gone, the incentive to negatively gear would be substantially reduced, which would in turn reduce the cost of housing, improve equity and redirect capital into “productive investment in things that actually grow the economy,” he says.

Anglicare’s Kasy Chambers argues that negative gearing should at least be allowed only for socially desirable development.

“Negative gearing should be for new builds, or builds in a certain area, maybe builds of a certain size, and limiting it to, say, the first 10 years of a house’s life,” she says.

But Hockey and the Coalition government are not listening. They argue specious economics in defence of the status quo. And the real reason for their intransigence is not economic, it is political: the rich rentiers vote for them.